This review is on the Prudential SurePath Annuity. The Purpose of this review is to show you where Prudential SurePath Annuity is strong and where it has weaknesses, so that you can make an informed decision, considering all available facts.

- Product type

- Fees

- Investment options that are available and their Realistic long-term investment return expectations

- Understanding the income rider

- How it can best help you as part of your financial plan

Prudential SurePath Annuity Quick Facts

| Product Name | Prudential |

| Issuer | Prudential Life Insurance Company |

| Type of Product | Fixed Indexed Annuity |

| Standard & Poor’s | “AA-” (Very Strong) |

| Phone Number | 1 (800) 778-4357 |

| Website | www.prudential.com |

There are a few ways that Agents might pitch this product.

- Combining the power of protection with growth opportunity

- No Annual Fees

- Create a lifetime guaranteed income that can increase over time

- Legacy protection for beneficiaries

How does this Annuity Work?

The Prudential SurePath Annuity offers you two different ways to potentially grow your money: (1) Index-Based Strategy and (2) Fixed Rate Strategy. Choose one or the other, or a combination of both. You decide the percentage to allocate to each. The performance of your chosen strategies is used to determine the amount of any interest credited to your contract.

The Index-Based Strategy, with this strategy your money will grow based on the change in the market index you choose. For this strategy SurePath offers you three indices to choose from, each with a Cap Rate or Participation Rate, also they give you the flexibility to choose the duration period of each strategy.

The Fixed Rate Strategy, this is a very conservative strategy and it does not give you any return associated with any index. So, the way it works is that Prudential will declare interest at the time of the purchase, it is not a fixed interest rate for every year and rates may vary upon renewal.

Within the investment choices we have:

- S&P 500® Index (1 or 3 years)

- MSCI EAFE Index (1 or 3 years)

- Goldman Sachs Voyager Index (1 or 3 years)

- Fixed Rate Strategy (1 year)

Important Note: Even though this Annuity does not have an annual fee, The Goldman Sachs Voyager Index includes does include an annual of 0.50% index fee, which accrues daily, meaning that a small portion of the fee is removed from the Index each day.

Welcome to AnnuityEdu where you can find unbiased annuity reviews, a perspective you can trust.

If it happens that you’re on this website for the first time. We’re dedicated to helping you with a second opinion viewpoint. To help you see through some of sales pitches that aren’t what they seem. We hope with the information we provide you’ll be better educated to make an informed decision before you buy.

Before we go in the details, here is an important legal disclosure.

This is an independent review at the request of readers. So they could see my perspective when breaking down the positives and negatives of this particular model annuity. This is an independent product review, not a recommendation to buy or sell an annuity. Prudential has not endorsed this review in any way, nor do I receive any compensation for this review. Before purchasing any investment product be sure to do your own due diligence and consult a properly licensed professional, should you have specific questions, as they relate to your individual circumstances. This is not meant to be specific advice. Your advisor may know more about your circumstances to make an appropriate recommendation. All names, marks, and materials used for this review are property of their respective owners.

Some information on Prudential

Prudential Financial, Inc. is an American Fortune Global 500 and Fortune 500 company whose subsidiaries provide insurance, investment management, and other financial products and services to both retail and institutional customers throughout the United States and in over 40 other countries. Prudential Financial is the largest insurance company in the United States, with total assets amounting to approximately 1.456 trillion U.S. dollars. Prudential is composed of hundreds of subsidiaries and holds more than $4 trillion of life insurance.

The best part about this annuity is…

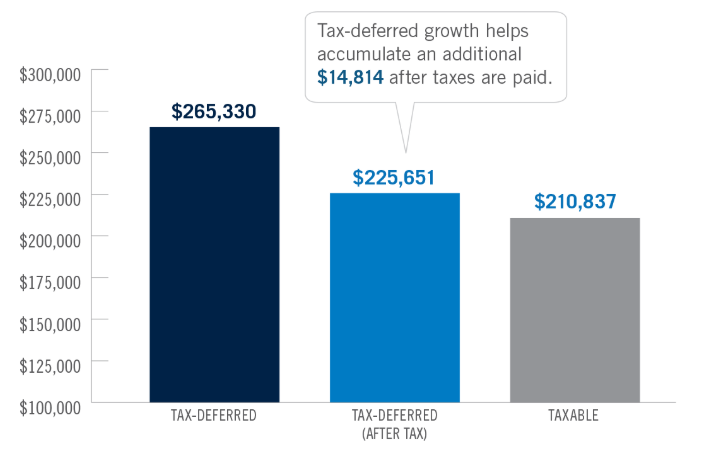

By far the best use of this Annuity is the tax deferral, so you will be earning interest on the money that you may have paid taxes on. Meaning this a good way to protect and grow your non-qualified money. Below there’s a graph for you to better understand how tax deferral works for this Annuity:

This annuity is a long term commitment with high penalties if you take you’re money out early.

The penalties are below.

| Contract years | 1,2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11+ |

| Withdrawal Charge | 9% | 9% | 8% | 7% | 6% | 5% | 4% | 3% | 2% | 0% |

What type of Performance can I expect from the options inside the Prudential SurePath Annuity ?

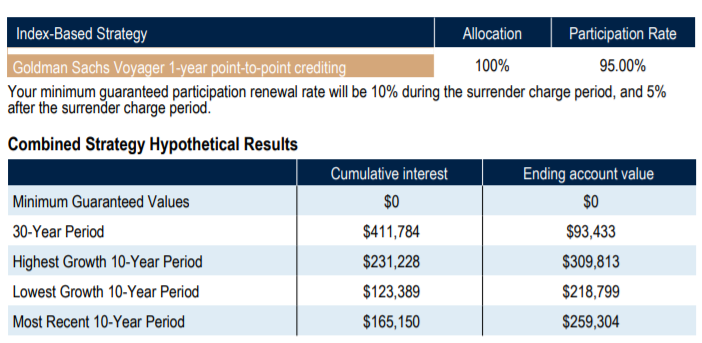

As an example, let’s suppose consideration John buys the Prudential SurePath Annuity for a total premium amount of $247,500 for a 30-year period. Assuming John chose the Index-based strategy with 100% allocation on the Goldman Sachs Voyager index 1-year point-to-point crediting period, the combined strategy hypothetical results shows:

For the Highest hypothetical growth in 10-year period there is an annualized return of 7.60% and a growth of around a 25% of the account value ($309,000). However, for the lowest growth 10-year period the result was a reduction in the account value to $218,000 (take into consideration that you principal is protected at the end of the contract) and for the most recent 10-year period the account value increead ton $259,304. Below there’s a table to better understand what this means.

How does the Point-to-Point crediting work for Prudential SurePath Annuity?

First of all let’s refresh what the Cap Rate and Participation Rate is and what it means for your Annuity.

The Cap Rate is the upper limit of interest that can be accredited at the end of a specific index term.

The Participation Rate is the percentage of any index increase use to calculate interest, in other words is how much of the interest earned by the index you are going to be exposed to.

For the Index based strategy in this annuity, the Point-to-Point is 1-3 years for any of the indices available. Let’s say the index that you chose earned a 20%, when interest ready to be credited your Cap Rate of 5% is the max amount you’re going to be accredited for that period. With the Participation rate assuming the same 20% of interest earned you’re going to be accredited with 35% of the index performance, meaning a 7% interest credited.

Annuity Edu’s Summary on the Prudential SurePath Annuity

Where it works best:

- If you have 7-10 years to defer income and want the ability to have increasing income

- producing a pension like lifetime guaranteed income stream that has the potential to increase

- Looking for conservative growth and want to have a guarantee on their principal

- Looking for an enhanced death benefit on the protected income value to pass money to beneficiaries.

- Guaranteed Principal Protection

Where it works Worst:

- For those who need liquidity

- For those not looking for guaranteed lifetime income

- For those looking for more upside potential in the market

My Insight

Overall, I think this annuity has some good features and some bad ones. The Annuity offers you Guaranteed Protection on your account value and tax deferral on your money, however I don’t think that’s a good reason to rush into this annuity. Buying an annuity is a long-term commitment and it’s important to test this annuity versus other top annuities in the marketplace to see which one fits your goals and objectives the most. This is something we do for free here at Annuityedu.com.

We’ll use our proprietary calculator to illustrate for you how this annuity will likely perform in your specific situation.

Click here to Test my Annuity, If your agent was honest with you, the numbers will match up – if not, well at least you know before you buy.

To Conclude

Unfortunately, I think advisers may be overestimating the returns you’ll receive. That’s why we can help you test the guarantee in your financial plan and for the internal rate of return it provides and see if your plan can handle it. This isn’t to say that having the Prudetial SurePath may not be a good way to meet your financial objectives with a portion of your dollars. It might, but it’s only possible after testing it that you’ll know.

Have Questions on Prudential SurePath Annuity? Have any comments?

Do you have any questions that you can’t seem to find the answer here on our website? [You can send us your questions here via our Free Annuity Help contact form].

We hope you found it helpful as you’re conducting your own research Prudential SurePath Annuity. We wish you all the best in your retirement journey!

If you have questions about this annuity, or you’re an investor that’s want to make sure your maximizing your retirement income. You can reach out to us through our contact form.

All the best,

AnnuityEdu.com