This review of the Annuity Allianz Legacy by Design is an independent review intended to show you where this Annuity is strong and where it has weaknesses. In order to make an informed decision, it is important to consider all available facts.

- Product type

- Fees

- Investment options that are available and their realistic long-term investment return expectations

- Understanding the income rider

- How it can best help your financial plan

- How it’s most poorly used as part of your financial plan

Allianz Legacy by Design Annuity Quick Facts

| Product Name | Allianz Legacy by Design |

| Issuer | Allianz Life |

| Type of Product | Fixed Indexed Annuity |

| Standard & Poor’s Rating AM Best | “AA” (Very Strong) “A+” (Superior) |

| Phone Number | 1-800-784-149 |

| Website | https://www.allianzlife.com/ |

Before we go into detail, here is an important legal disclosure.

This review of Allianz Legacy Design Annuity is an independent review at the request of readers. Intended to explain my perspective when breaking down the positives and negatives of this particular model annuity. This is an independent product review, not a recommendation to buy or sell an annuity. Allianz Life Insurance Company has not endorsed this review in any way, nor do I receive any compensation for this review. Before purchasing any investment product be sure to do your own due diligence and consult a properly licensed professional, should you have specific questions related to your circumstances. This review is not intended to give specific advice and your adviser may know more about your circumstances to make an appropriate recommendation. All names, marks, and materials used for this review are property of their respective owners.

Before we go into the review, some information on Allianz

Allianz Life Insurance Company of North America (Allianz) is a leading provider of retirement solutions, including fixed and variable annuities and life insurance for individuals. Variable annuity and variable life insurance guarantees do not apply to the performance of the variable subaccounts, which will fluctuate with market conditions.

You can learn more about this from https://www.allianzlife.com/

How do Agents Typically Pitch This Product?

- 25% death benefit bonus.

- Create an inflation-adjusted asset protection

- No fees

- Tax-Deferred accumulation

How this Annuity Really Work?

Allianz Legacy by Design is a combination of two FIAs. First, we have the Allianz Legacy Planner Annuity, which is funded with qualified money. Then, when the RMDs from this annuity are available, you have two options: 1) It can go directly to you. 2) You can contribute the RMDs to the second annuity of this combination, which is the Allianz Legacy Plus.

The Allianz Legacy Planner Annuity is a fixed index annuity funded with your qualified assets, for example, your Traditional IRA and Sep IRA. However, not everything in this annuity is perfect, one of the downsides is that there’s no minimum free withdrawal, so in case you need to withdraw money for an emergency then you will have to face the surrender charges for this annuity, for this reason, I believe the Allianz Legacy Design would be more beneficial only to those who just want to ensure a legacy for their relatives and protect their capital against inflation.

When the RMDs are available for this annuity the person has the option to transfer the after taxed RMDs to the second annuity, the Allianz Legacy Plus. This annuity has some good features available such as tax-free growth since all taxes were withheld from the RMDs from the first annuity, also Allianz pays a 25% death benefit in order to serve as a protection for the capital.

This annuity is a long-term commitment with high penalties if you take your money out early.

The penalties are below.

Surrender charges

| Contract years | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11+ |

| Withdrawal Charge | 9.3% | 8.4% | 7.5% | 6.6% | 5.7% | 4.75% | 3.8% | 2.85% | 1.9% | 0.95% | 0% |

There are no fees for this annuity, however, you don’t have a minimum free withdrawal each year as most annuities have. Which means that from the Allianz Legacy planner you can’t withdraw any money without having to address the penalties showed above. Nevertheless, when the RMDs go to the Allianz Legacy Plus Annuity you have no limit tax-free withdrawal amount.

What are the Cap rates for the Allianz Legacy by Design Annuity?

Below we can see the Indexes and the current rates for this annuity:

| Indexes | Legacy Planner | Legacy Plus | Current Rates |

| Nasdaq-100® Index Monthly Sum with a cap | 10% | 10% | 1.10% Cap |

| Nasdaq-100® Index Annual Point-toPoint with a cap | 10% | 10% | 1.25% Cap |

| Russell 2000® Index Monthly Sum with a cap | 10% | 10% | 1.10% Cap |

| Russell 2000® Index Annual Point-toPoint with a cap | 10% | 10% | 1.25% Cap |

| Bloomberg US Dynamic Balance Index II Annual Point-to-Point with a cap | 10% | 10% | 1.25% Cap |

| Bloomberg US Dynamic Balance II ER Index Annual Point-to-Point with a participation rate | 10% | 10% | 35% Par |

| Bloomberg US Dynamic Balance Index II Annual Point-to-Point with a spread | 10% | 10% | 6% Spread |

| PIMCO Tactical Balanced Index Annual Point-to-Point with a cap | 10% | 10% | 1.25% Cap |

| PIMCO Tactical Balanced ER Index with a participation rate | 10% | 10% | 35% Par |

| PIMCO Tactical Balanced Index Annual Point-to-Point with a spread | 10% | 10% | 6% Spread |

What type of Performance can I expect from the options inside the Legacy by Design Annuity?

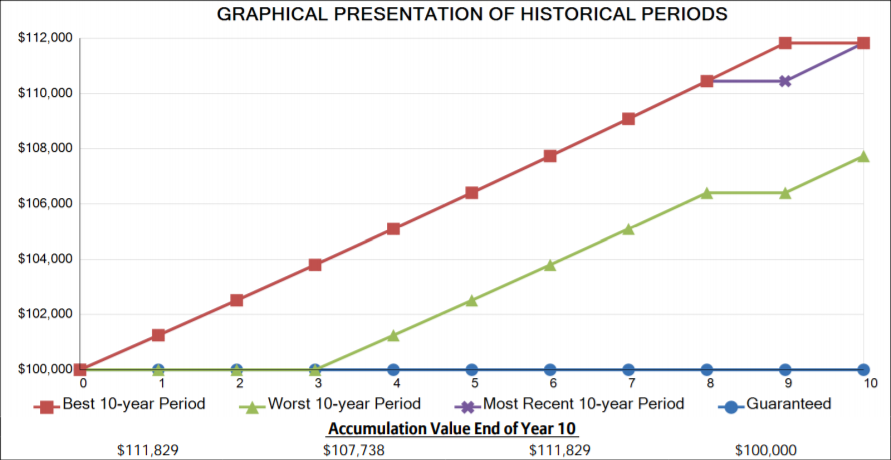

To understand the guaranteed values that you can expect from this annuity, let’s see this example, covering a 30-year period with the two annuities combined, this is what would happen if the indexed allocations earn zero interest and the fixed allocations earn the minimum annual fixed rate of 0.10% in all years.

With a premium of $1,000,000 Andrew purchased the Legacy by Design annuity for his son Michael. Assuming Andrew did not cash out any of the RMDs and instead transferred it to the Legacy Plus annuity, at the end of the 30 years the guaranteed minimum value will be around $952,174 with 0% interest. However, when it comes to the total death benefit Andrew will have $1,100,699 taking into consideration the 25% death benefit bonuses that took place every year RMDs were transferred to the Legacy Plus.

Please remember this a hypothetical scenario where the interest return is 0%. In the most recent 10-calendar years the return with caps for this combined annuity was around 1.54% previously shown values would be higher than with the 0% return.

Below I want to show you a graphical presentation of the historical periods so you can better understand the hypothetical returns that I just mentioned.

Where does it work best:

- Safety of principal

- Conservative Growth

- Those looking for legacy

- Death benefit bonus

- Protection against inflation

Where does it least work:

- Those who need 100% liqudity

- Those who need prefer a Tax Free Death Benefit

- Those looking for guaranteed lifetime income

Annuity Edu’s Summary Allianz Legacy by Design Annuity

Overall, I think this Fixed Indexed annuity has some good features. The annuity has strong fundamental characteristics for those seeking a guaranteed and protected inheritance for their beneficiaries.

However, buying an Indexed Annuity is a long-term commitment. It is important to test this annuity versus other similar annuities to see which one fits your goals the best. Often, these annuities earn nowhere near the return it says it earns, so this is something to pay really attention when it comes to evaluating an annuity, in that event, if you’d like to know how much is the real interest your annuity is earning you or how much upside potential can it give you, we do this for free here at Annuityedu.com. Test the annuity to know if it is a good fit for you. We’ll use our proprietary calculator to illustrate how this annuity will likely do in your specific situation.

To be sure, Click here to request a complimentary, no obligation Annuitycheck® Report to test an existing annuity or an annuity before you buy. If your agent was honest with you, the numbers will match up – if not, well at least you know before you buy.

To Conclude

Unfortunately, advisers tend to underestimate how low the returns are over time, especially when omitting the caps and real rates of the annuity. The return of Annuities is comparable to the return of a bond more than a stock. It’s about having realistic expectations and risk/adjusted basis. That’s why we can help you test the guarantee in your financial plan for the internal rate of return Allianz provides and see if your plan can handle the amount of return in retirement.

Furthermore, purchasing an annuity is often an irreversible decision. You’ll have high surrender fees if you change your mind after you buy it. Surrender fees cause assets to not be used at their fullest potential.

Have Questions on the Allianz Legacy by Design Annuity? Have any comments?

Finally, if you need clarity about the Allianz Legacy by design or you have any questions and you can’t seem to find the answer here on our website [You can send us your questions here via our Free Annuity Help contact form.] You can also reach out to us by email or by phone.

We hope you found it helpful as you’re conducting your own research on the Allianz Legacy by Design Annuity. We wish you all the best in your retirement journey!

All the best,

Annuityedu.com